Let every man divide his money into three parts, invest a third in land, a third in business and a third let him keep in reserve.——- Talmud ( 1200BC—AD 500 )

The idea of asset allocation was very much present even 2000 years ago. In other way we can say that the concept of risk management was also familiar at that time. In modern times the concept of portfolio and risk management got a new dimension with the introduction of Modern Portfolio Theory ( MPT ) by Harry Markowitz. According to modern portfolio theory it is not enough to invest in different type of asset to reduce risk. Investor should also know whether there is any relationship among the invested asset class return. The nature and strength of the relationship among the invested asset class is the most critical issue in asset allocation. The focus on investment policy and asset allocation is transforming investment management.

Among the various investable asset class, real estate is one of the most preferred asset class among the investors since the ancient times. There are various forms or avatars of real estate investment. With time some type of real estate investment became obsolete with the introduction of new avatar. Like our great grandfathers used to consider investment in agricultural land as the best possible investment opportunity. But with time that concept changed. In early 2000 buying multiple residential property was a very lucrative investment opportunity. Unfortunately, with time, it seems that the glitter is no more there. We are not trying to say that real estate is a bad investment asset class. The fact is, low correlation of return between real estate investment and other asset class investment helps to reduce the total risk of the portfolio. What is being conveyed here is that the preferred form of real estate investment is changing across the world due to change in taste and preference. We do need real estate for our residential purpose but buying physical real estate for investment purpose will be less preferred option due to various execution barrier, such as quantum of investment, high transaction cost, poor liquidity, chances of fraud and litigation etc. With digitisation, investment in physical form of asset is becoming obsolete. The present generation demands mobility & flexibility and hence, investment in asset class which can be very easily liquidated will be more and more preferred. And here comes the new digitised avatar of real estate investment known as REIT i,e Real Estate Investment Trust.

Structure of REIT

REIT i.e., Real Estate Investment Trust as a concept was first introduced in United States in 1961.In India the REIT concept was first introduced by SEBI in 2013-2014. The objective was to increase transparency and liquidity in the Indian real estate market.

Real estate investment trust is an investment vehicle regulated by SEBI, that own and manage a portfolio of properties. The structure of REIT is similar to the mutual fund structure. Mutual funds hold and manage a portfolio of equity, debt, and money market instruments by collecting funds from the investors. REITs invest in a portfolio of real estate assets in various forms such as commercial complexes, office towers, shopping malls, IT parks, etc by collecting funds from investors. Units are issued to the investors against their investment and listed on the stock exchange platform. There is a sponsor who brings in the capital to set up the REIT. It holds minimum 25% shares of REIT for the first three year and after that it can be reduced to 15%.The AMC or the asset management company is responsible for investment management. The trustee ensures that the money is managed in the interest of the shareholders. The Trustee holds the Real Estate Assets of the Trust in its Trusteeship, and these assets are no longer directly controlled by the Sponsor. In simple words a REIT unit represents part ownership of the Real Estate Assets held by the Trust and this entitles the unit holder, a share of the income generated by the REIT.

Source of income generation :

All the REITs in India need to adhere the following SEBI mandated guidelines.

At least 80% of the investments made by a REIT must be in completed commercial projects that can be rented out to generate regular income. Hence rental income is the major source of revenue of REITs

The remaining assets of the trust can be held in the form of stocks, bonds, cash, or can also be invested in under-construction commercial property ( Max 10% ).

Investment Benefits & Risk:

The following are some key benefits of investing in REITs:

Diversification: Investment in REITs help to diversify the portfolio through exposure in Real Estate, without the hassles related to owning and managing commercial property.

Low Ticket Size: REITs require small initial investment of Rs. 50,000 or a minimum lot of 100 shares ( whichever is higher ) to get an exposure to commercial real estate.

Professional Management: Venturing in commercial real estate through REIT route is safer because REIT investments are managed by professionals.

Regular Income Generation: REITs generate income from rental collections and are required to mandatorily distribute 90% of this net income to investors as dividends. Hence it helps to create a regular source of income.

Capital Gain: Since REITs are listed entity scope of capital gain will also be there.

Liquidity: REITs are listed and traded on Stock Exchanges hence investors can exit their investments if required.

Risk:

REITs are listed and traded in stock exchanges. Hence price may be volatile due to short term demand and supply. But price volatility of REIT units will be much lower compared to normal shares. If the investor is forced to sell the units at a price lower than the purchase price due to some emergency, in such a scenario the investor may incur loss. This risk can be managed by increasing the investment time horizon in this instrument with a maximum allocation limit.

If properties remained vacant for long period reduction in rental income is also a possibility which may reduce the dividend pay-out. Although that probability is low. Because in a growing economy demand for commercial real estate is high. Although investors need to be careful about the real estate portfolio of the REITs.

Global Trend & Indian Scenario

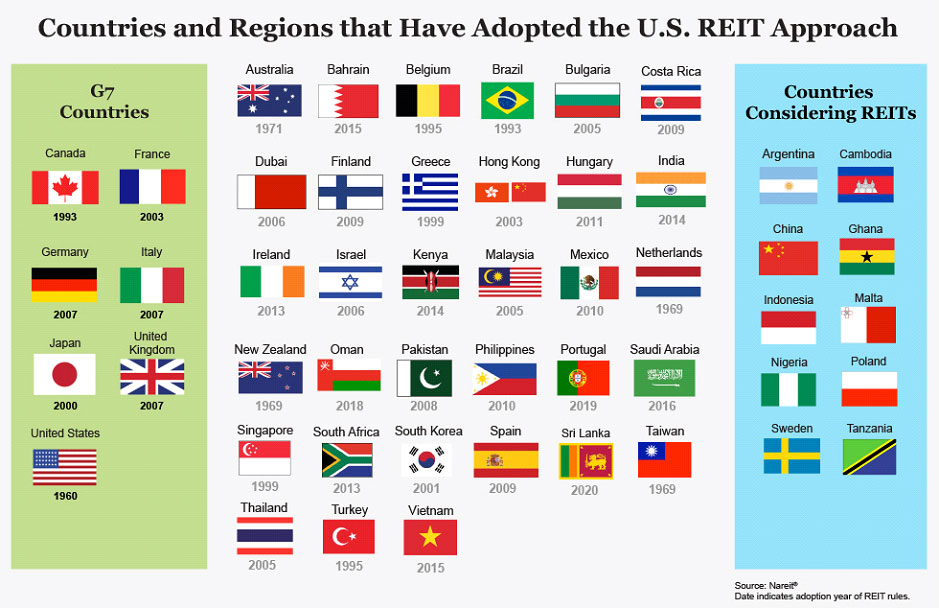

Forty countries including all G7 countries have adopted the U.S.-based REIT approach to real estate investment, offering all investors the access to portfolios of income producing real estate across the globe.

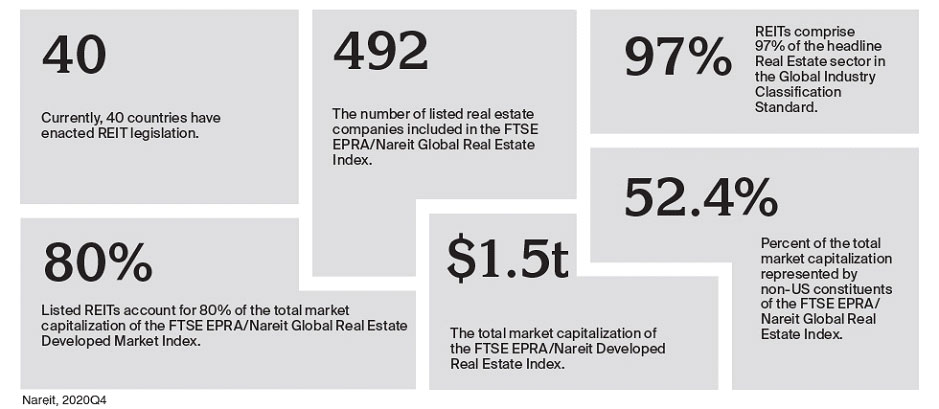

The cumulative market capitalization of REITs globally is more than $2 trillion, as 40 countries now have active REIT legislation including 25 nations with at least one actively traded REIT. The next wave of growth is likely to be driven by non-traditional property sectors in the mature U.S. and European markets and the emergence of listed real estate sectors in high-growth Asian markets.

In Asia, several markets are poised for growth. Singapore, with its REIT market cap approaching $70 billion USD, also merits attention. Interestingly, most Singapore-listed companies own assets outside of the country. That makes Singapore’s REIT market a unique avenue for real estate owners around the globe, to list on a public exchange and access new investors, including high net worth and institutional investors in Asia.

Opportunity in India

India’s nascent REIT regime is expected to offer the opportunity to invest in stabilized institutional-quality real estate in India for the first time. The real estate companies currently listed on the Indian stock exchange are primarily condominium developers that have seen boom-and-bust cycles and offer a quite different risk profile than the stabilized real estate of REITs. According to JLL the global real estate service firm “ India’s current office markets across seven major cities have a potential space of 284 million sq. ft that could be securitised with an estimated value of $36 billion. Currently there are only 3 REITs that are traded on exchanges–Embassy Office Parks, Mindspace Business Parks and the recently listed Brookfield India Real Estate Trust.

The relative stability of income from REIT property portfolios is likely to find a home in the investment portfolios of domestic insurance companies, pension funds, and mutual funds over time.

Taxation

Dividend : Any dividend or interest earned from REITs is completely taxable in the hands of the investor according to the applicable slab rate. The government later amended the announcement, but with a caveat. Now, if a REIT opts for a lower corporate tax rate of 22% instead of 30%, the dividend will be taxable in the hands of investors. However, most REITs have opted for a higher rate of corporate tax, therefore, the dividends will be tax-free in the hands of the investors.

Capital Gain: The units of REITs shall be regarded as long-term capital assets if the same are held for a period of more than 3 years. If held for a period of less than 3 years, then such units will be regarded as short-term capital assets.

In case units are held as a capital asset by the holder, gains arising on sale of the REIT units will be liable to tax as under:

i. Long-term capital gains exceeding INR 1 lakh on sale of units held for more than 36 months – 10% (plus applicable surcharge and cess) as per section 112A of the Act; and

ii. Short-term capital gains on sale of units held for up to 36 months – 15% (plus applicable surcharge and cess) as per section 111A of the Act.

Since this is an evolving asset class in our country there can be frequent change in tax rules. Request the readers to consider the latest tax guidelines as and when they decide to invest.

Covid Impact on Commercial Real Estate Sector

Across the world companies that own office buildings and hotels, or those that lease space to restaurants, bars, department stores and other retailers, have been hit extremely hard last year. The distribution of COVID-19 vaccines is fuelling optimism in the developed world, that people will increasingly return to the ways they used to shop, travel and work before the pandemic.

In US the national unemployment rate fell from 6.2% to 6% in March 2021 and employers added 916,000 jobs, the most since August. That included 216,000 positions at restaurants, hotels, and bars — the sector most damaged by the pandemic.

According to the International Monetary Fund forecast in April 2021, U.S. economy will grow 6.4% this year, which is the fastest annual pace since 1984 and the strongest among the world’s wealthiest countries.

So far this year, the commercial real estate market has seen some positive trends. Many businesses that had to shut down or operate on a limited basis are being given the green light to open by governments amid a pullback in new coronavirus cases and a ramped-up rollout of vaccines.

In India due to Covid second wave the present situation may not look very promising at the ground level. Commercial real estate is having a tough time since last year. But all is not bad. According to a survey report done by one of the leading property consultants, nearly 90% of the respondents said that they miss their office environment, while working from home. Apart from this, the recent update of office spaces in leading cities, including Mumbai and Bengaluru, have suggested that demand is looking up. Most of the leading technology companies have renewed their office leases. Accenture, Oracle, IBM, TCS, Microsoft and many other domestic companies have renewed their lease agreements which cover over 3.5 million sq ft of office space in the top four cities, such as Bengaluru, Hyderabad, Pune and Mumbai.

The fact is, if we can look beyond the current situation and believe that we will get back to normal life in coming years as suggested by current global data ( discussed above ), then there is reason to believe the current situation maybe temporary and we are headed for brighter days ahead.

Someone said in some context that the most important mantra of successful investing is to buy the asset when price is low because of some gloom and doom situation. And sell when price is higher as the days are sunny & bright. Can’t say whether it is applicable here or not, — YOU ARE THE BEST JUDGE!!

Summary & Conclusion

The above discussion can be summed up as follows.

⦁ Real Estate Investment Trust is a popular investment vehicle across the world since last 50 years. In India it was introduced in 2014. REITs in India own and manage a portfolio of properties by collecting funds from the investors and regulated by SEBI.

⦁ Units are issued to the investors against their investment and listed on the stock exchange platform to provide liquidity.

⦁ At least 80% of the investments made by a REIT must be in completed commercial projects that can be rented out to generate regular income. Hence rental income is the major source of revenue of REITs.

⦁ REITs generate income from rental collections and are required to mandatorily distribute 90% of this net income to investors as dividends. Hence it helps to create a regular source of income which is tax free in the hands of the investor.

⦁ If units are sold before 3 years, then 15% capital gain tax will be charged on the profit amount.

⦁ If units are sold after 3 years, then 10% long term capital gain tax will be charged on the profit.

⦁ If properties remained vacant for long period reduction in rental income is also a possibility which may reduce the dividend pay-out which can be considered as a risk.

⦁ In the near-term price may be volatile due to short term demand and supply.

⦁ In terms of risk return profile REITs as an asset class should be placed after debt instruments and before equity.

In India REITs are relatively new investment concept and at a very nascent stage. Globally REITs are more than 50 years old concept and historically have delivered competitive total returns, which includes steady dividend pay-out and long-term capital appreciation. They are excellent portfolio diversifier as REITs are comparatively less corelated with other asset class that can help reduce overall portfolio risk and increase returns.

Disclaimer :

Considerable care has been taken to prepare the above report. Although it may be possible some data error might be there. Readers are suggested to cross check any data if required.

This report is not some advice to buy, sell or perform any investment related activity. Please consult your investment adviser regarding any such activity.