Executive Summary

- Economies across the world are gradually getting back to normal life with the increased pace of vaccination.

- Unprecedented fiscal and monetary policy measures taken by the governments and central banks flooded the system with liquidity. Increased spending on infrastructure, ultra-low / zero interest rate, continuous bond purchase and direct cash transfer to the consumer brought back the demand in the system.

- Fear of covid, continuous weather disruption in many countries, disruption in the shipping lines, scarcity of labour, wage hike is also creating supply side hazards.

- Continuous rise in price of the raw materials such as oil, gas, aluminium, copper, basic food articles forcing the producers to increase the price.

- All the above forces pushing the economy towards high inflationary environment. Central banks including US federal Reserve, RBI in India believes such high inflation will be transitory. The actions of the policy makers will not be pre-emptive as stated, and they want to act only on the evidence of sustained long term high inflationary environment. At present the best-case scenario is inflation will shoot up but may not sustain. And not so preferred scenario is there will be a change in long term inflation expectation.

- After a prolonged era ( almost 30 years ) of benign inflation in US, any upward revision in the long term inflation expectation will create imbalance in the world economic system and trigger fast asset price correction. Emerging markets including India may also feel the heat. Investors need to be careful about their asset allocation in the portfolio and may look for rebalancing if required.

INFLATION, may be one of the most used economic term in our daily life. It is most used because it impacts the financial budget of almost all section of the population —from the basic household expenses to allocation of resources by the corporates as well as governments. Rate of increase in price of goods and services over a certain period is termed as Inflation. Inflation up to a certain level is a good sign for the economy as inflation also signifies demand. Economists believe that low, stable, and—most importantly—predictable inflation is good for an economy. But rapid increase in average price level resulting from higher demand and higher cost creates an inflation spiral.

Pressure on the supply side of the economy can be inflationary and may lead to ‘cost-push’ inflation. Production can be disrupted due to disruption in the supply chain caused by natural disasters, shortage of labour and raw materials . Continuous increase in oil price and other commodities can lead to cost push inflation. On the other hand, demand and economic growth can also be boosted by loose monetary policy of central banks by infusing liquidity in the system through asset purchase program and keeping interest rate exceptionally low for a prolonged period of time. Extra ordinary government spending, continuous rally in asset prices may also create demand shocks for a certain period. If this sudden increase in demand exceeds economy’s production capacity the resulting strain is reflected in demand pull inflation. Sometime high-level inflation is cost push or demand pull but it can also be caused by both which can cause a real pain for the policy makers.

Since the beginning of March 2020 till now, is one of the most difficult periods faced by the central banks and government policy makers to manage the economy from the covid impact. Major central banks across the globe reduced interest rate to exceptionally low or zero and initiated extraordinary amount of bond purchase program to infuse liquidity in the system. Government authorities pumped money by directly crediting the bank account of the citizens. Corporates got support from the central banks and governments to maintain the business continuity. All these activities were targeted to restore the purchasing power of the consumer and keep rotating the economic activity as much as possible keeping in mind the covid situation. As more number of people are getting vaccinated and countries trying to get back to the normal, spending across the world is increasing and pumping the demand. Please remember this happening across the world not in one or two countries, may be at a different pace.

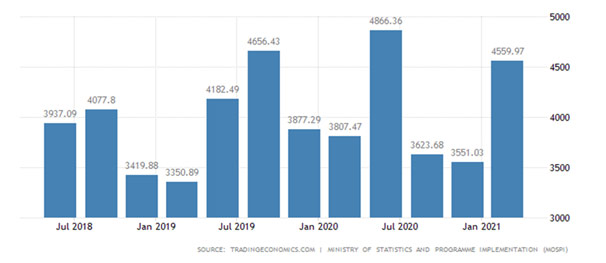

Government Spending in India increased to 4559.97 INR Billion in the first quarter of 2021 from 3551.03 INR Billion in the fourth quarter of 2020.

Infrastructure output in India jumped by 56.1 percent year-on-year in April of 2021, accelerating from an upwardly revised 11.4 percent rise in the previous month. It was the biggest gain since series began in 2005. Infrastructure output in April of 2020 had contracted sharply amid the coronavirus pandemic.

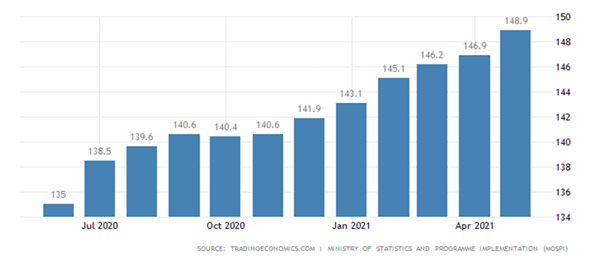

The transportation sub-index of the CPI basket in India increased to 148.90 points in May of 2021 from 146.90 points in April of 2021. Indicating increased activity in transportation.

Source: Ministry of Statistics and Programme Implementation (MoSPI)

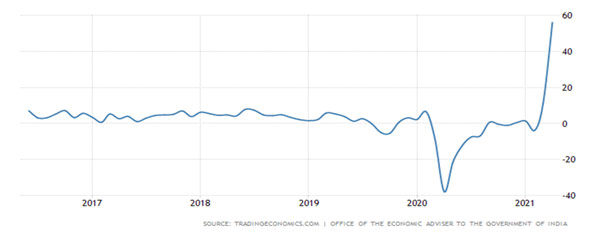

Impact of the above developments is also reflected in the Indian GDP numbers. Gross Domestic Product (GDP) in India expanded 7.90 percent in the fourth quarter of 2020 over the previous quarter.

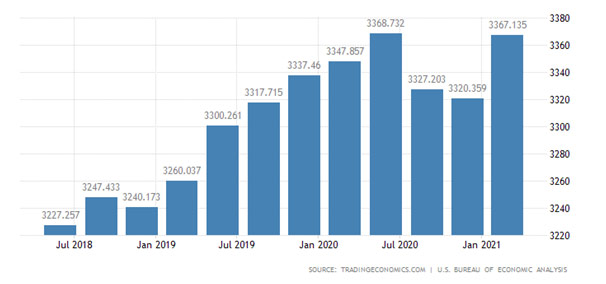

In US also we have the similar picture. Government Spending in the United States also increased to 3367.14 USD Billion in the first quarter of 2021 from 3320.36 USD Billion in the fourth quarter of 2020.

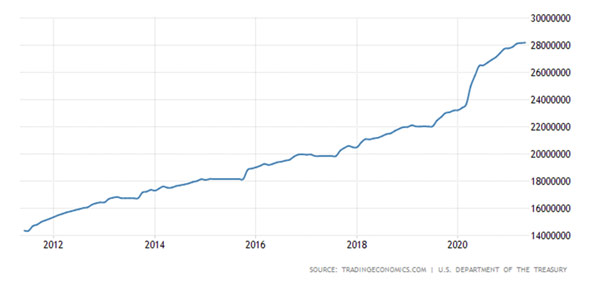

Government Debt in the United States jumped to 28199008 USD Million in May from 23574714 USD Million in March of 2020.

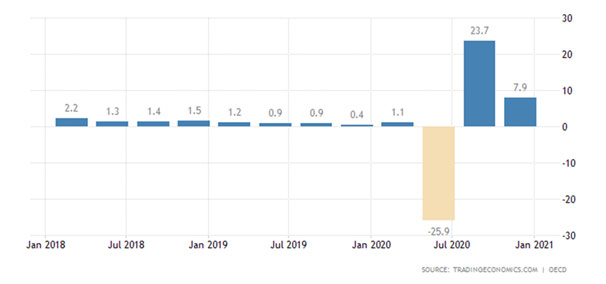

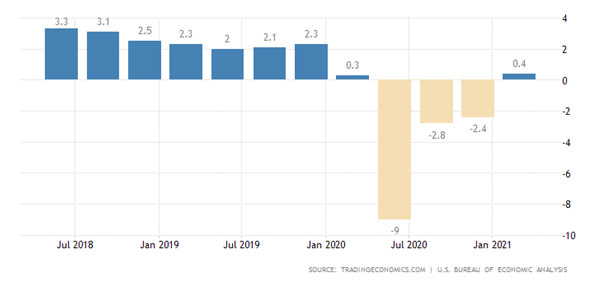

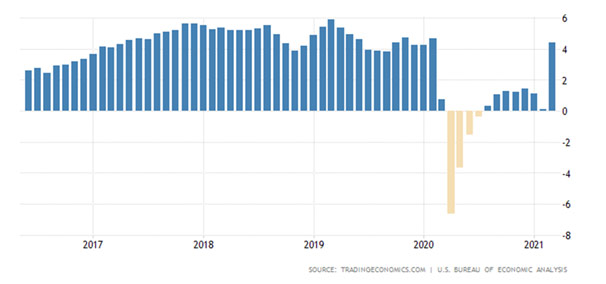

The Gross Domestic Product (GDP) in the United States expanded 0.40 percent in the first quarter of 2021 over the same quarter of the previous year.

On the supply side some behavioural change is being observed among the labours in many developed and developing countries including India. Labours are very reluctant to get back to work. Major reasons being fear of covid, uncertainties regarding lock down and financial support provided by the governments during this period. Industries in US are facing serious labour problem disrupting the production. Similar situation is faced by many other countries as well.

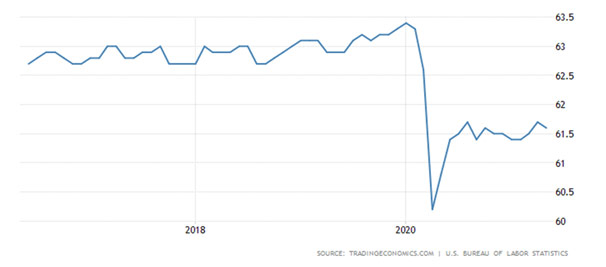

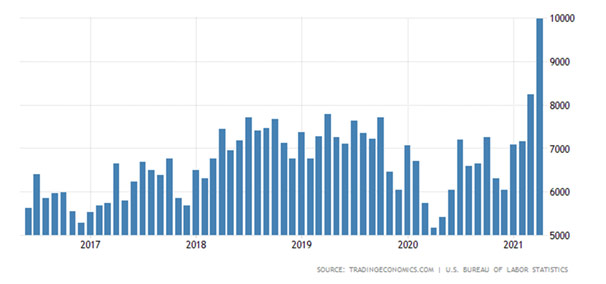

Labour force participation rate in the US edged down to 61.6 percent in May 2021 and has remained within a narrow range of 61.4 percent to 61.7 percent since June 2020.

At the same time Job Vacancies in the United States increased to 9982 thousand in April from 8237 thousand in March of 2021.

Wages in the United States also increased 4.41 percent in March of 2021 over the same month in the previous year.

Along with labour shortage and wage hikeprices of production raw materials are also shooting up.

Crude Oil

Oil Price rebounded sharply in last one year and now trading at a 2 year high. In India petrol & diesel price already crossed 100/litre mark.

Copper price is trading at a multi-year high

Aluminium Priceis also trading at all time high

Chinese regulator has already started reacting to such high commodity prices by banning speculative derivative activities. It is also planning to release metal reserve in an effort to tame commodity rally. But how effective will those measures be, only future will tell.

Thompson Reuters Commodity Price Index

Below is the Thompson Reuters commodity price index which tracks the price movement of 19 major commodities which includes agricultural commodities, minerals, metals, crude oil etc. Post 2009 commodity prices across the globe was in a correction mode due to recession and excess supply. But from 2020 June onwards it started rising and broke the10-year-old primary trend line. Currently it is trading at a 5 year high

Baltick Dry Index

The above picture shows the movement of BALTIC DR INDEX which is reported around the world as a proxy for dry bulk shipping stocks as well as a general shipping market bellwether. It can be observed that the correlation is very direct with economic activity. During the period of strong economic growth between 2003—2008 the index was rising but post 2009 i.e after recession the index was continuously moving in range for last 10 years. Presently the index broke out of the highest range of last 10 years. Supporting our growth picture and as well as the inflation picture.

Now the question is whether such labour issue and the measures taken by the global central banks and the governments across the world during the same time horizon to protect the economy from covid impact will lead to inflationary environment.

Inflation in US

Annual inflation rate in the US accelerated to 5% in May of 2021 from 4.2% in April and above market forecasts of 4.7%. It is the highest reading since August of 2008.

Inflation in India

Annual consumer inflation rate in India increased to 6.3 percent in May of 2021, the highest in 6 months, from a downwardly revised 4.23 percent in April. Figures came well above market forecasts of 5.3 percent, as higher global commodity prices including including crude, edible oils and gold weighed.

From the above discussion we find out that one of the major risksthat may spoil the growth party is sustainable high inflation which was discussed in April 2021 article. If inflation moves within the expected range of the central bank, it is not a threat. If it breaks out of the range with a huge thrust and backed by higher cost and higher demand, then it is likely to be sustainable. There is also the logic that higher prices are their own best cure. Once consumers have spent their savings pile, higher prices will restrict demand unless pay/wage goes up to match.

At this point major central banks including RBI believe that highinflation will be transitory means it will be only for a short period hence major policy change is not required. Well, that is the best-casescenario, and we all want that. But if it does not happen then it may create a lot of imbalances in the economic system across the world. US Federal Reserve will have to reduce the pace of the bond purchase programme and finally may have to raise rates after decades. If that happens asset prices will correct across the world. Fast moving money from emerging economymay go back from where it has come from because the opportunity cost may change due to rise in interest cost.Please remember, asset prices will not correct when the rates will go higher but it will react as soon as the market participants will smell a higher probability of rate hike along with federal reserve reducing bond purchase. In this context would like mention that a question might come to our mind that why we are so much discussing about US economy and the action of US Federal reserve. Because they matter. Policy of US federal reserve along with European central bank are the major drivers of asset prices across the world. The present rally in the equity market across the world is driven by the 25000-billion-dollar liquidity provided by these central banks. We like it or not but that is the fact. Any smallest indication towards change in policy by these Central banks will be treated very seriously by the financial market participants.

Now the final question is, how do investors will position their portfolio in the above scenario.

Asset Class Behaviour

Before we get into the above discussion, it is important to understand how asset prices behaveduring the periods of high inflation.

If high inflation ( Beyond the expected range of Central Bank ) persists for long period then it will impact thefixed income asset class negatively. Bond yields will start risingand bond price will fall, which will negatively impact the high duration bond the most. Once interest rate starts moving up gradually,beyond a certain point, high interest rate will also impact the profitability of the company.

Normally during the initial phase of high inflation equities& commodities do well which is happening at present. But beyond a certain point,sustainable high inflation will impact the purchasing power of the population thus negatively impacting the topline and bottoline of the companies.

Historically Goldperformed well during the phase of high inflation and considered as a hedge against inflation.

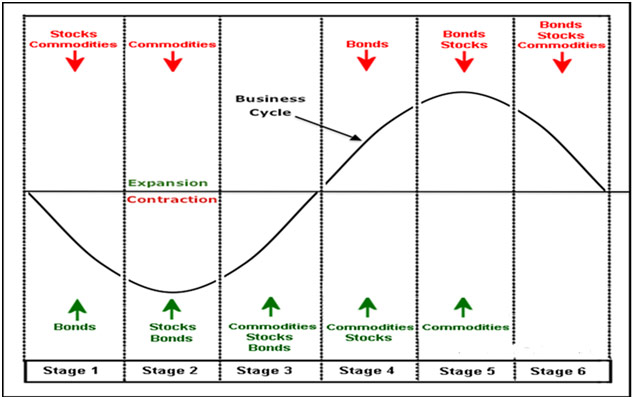

The diagram below will help you to understand the behaviour of the asset class across different economic cycle and where do we stand at this point of time. Near the pick of the expansion phase of the economy inflation starts rising.

Business Cycle & Asset Class Relation

Please remember, this is just a guidance how asset prices may behave during high inflation. Investors should not use it as an advice to buy and sell assets without consulting their investment advisors.

Portfolio Positioning

Investment portfolios are created keeping certain conditions in mind. The risk profile, objective time horizon, and the return objective of the investor is the most important elements to consider. Along with that the present valuation of the market, positioning of economic cycle also plays an important role.

Once the portfolio is created there are various approach to manage the portfolio. One approach is to ignore all the risks that create near term volatility in priceand impact the portfolio.It suggests holding the portfolioaccording to your objective time horizon. The basic reasoning behind this philosophy is all will be fine in the long run. Since economy moves in cycle ( up & down ) such assumption holds good in the long run,at least historically. In this context investor should also understand very clearly the definition of long run and whether it is matching with his / her objective time horizon.If for some reason all is not well at the end of the investment time horizon price, it may be a nasty surprise.

Another style suggests managingthe portfolio asset allocation tactically, to handle the near term risk or take the better advantage of the near term opportunity keeping in mind the broader objective. This is an active management process. It requires in depth understanding of the economic cycle, market valuation, risk management etc.

Investors may choose any of the above process depending on the suitability.Periodical review of the portfolio and rebalancing of the portfolio asset allocation is always advisable to the investors who follows the buy & hold approach. There will be phases in the market when the conviction of both type of investor and the advisor will be tested very heavily. When the market goes up continuously for a long period of time it increases the risk appetite of the investor. They start believing that it is a foolish decisionnot to have an aggressive portfolio irrespective of the risk profile. The funny part is, this will not be the conscious decision of the investor and he will be pulled in by the strong price movement to get into such conclusion. And when the price goes down heavily it reduces the risk appetite of the investors and they become ultra conservative. Again, price forcing the investors to move away from the original risk profile.Both the behaviour will impact the portfolio asset allocation hence thefuture performance. It is advisable not to change the investment management philosophy suddenly.

If you belong to the camp who constructs the portfolio by allocating fund to different asset class, based on the risk appetite, objective time horizon and return objective and believe in passive management ( Buy & Hold )then you can safely ignore the current development and its impact on the portfolio. Just sit tight and don’t loose conviction on your management philosophy once challenged my the market.

If you belong to the camp, who strategically allocates fund to different asset class, based on the risk appetite, time horizon and return objective and believe in active management process to handle the short term risk, and also to take advantage of the short term opportunity by managing the asset allocation tactically keeping in mind the long term objective —it is time to be active.

Please remember investment management is a professional activity and should be backed by relevant education, knowledge, experience, and wisdom. Whether passively managed or actively, investors must take a professional approach towards his/her investments. And it starts with getting hold of such a person who will hand hold you in this long journey by guiding you to take the correct decision.

Conclusion:

Massive spending plans by major developed economy and accommodative policies by central banks across the world has stoked inflationary concerns. Longer-term price pressures on commodities and supply chains remain, including companies potentially shifting more production to domestic sites. Furthermore, the Fed’s new policy framework is no longer pre-emptive, meaning officials want to let inflation run above target for some time, to compensate for undershooting for so long in the past. Though the short-term outlook is coming into view, there’s elevated uncertainty when it comes to longer-term inflation. After investors have experienced a prolonged era of benign inflation, portfolios may be underprepared for even relatively modest changes in both inflation and inflation expectations.

Disclaimer :

Considerable care has been taken to prepare the above report. Still it may be possible some data error might be there. Readers are suggested to cross check any data if required.

There are many other economic indicator or variables which can be used to study the economic activity like IIP DATA, Service Sector PMI etc. But the variables we considered here mostly captures the impact of the others. And most importantly tried to keep the report simple as much as possible.

This report is not some advice to buy, sell or perform any other investment related activity. Please consult your investment adviser regarding any such activity.